Believe And Budget

Money Talk with The Maloneys

How I paid off 32k of Student loan debt fast!

This post may contain affiliate links, and they are no cost to you!

I went to a private school my first year of college. I will admit I took out student loans because it was the thing to do. It was okay. It was “NORMAL.” I played soccer on a scholarship and went out of state. It really did not help me in the financial world.

I was lucky to have my older sister tell me, just “transfer to an in state university and live with me for free to take out less loans.” Luckily, I listened, I lived with her for a year then did something stupid again. I lived back on campus in an expensive individual dorm. Next, I did something even worse lived by myself in my own apartment because I had an “adult” job.

So, here we go…I wanted to kill my student loans. I built my net worth to be -$32,000 in 2014!

Here is what I did and you can do it too to build your net worth to be positive instead of negative!

Put your mind to it!

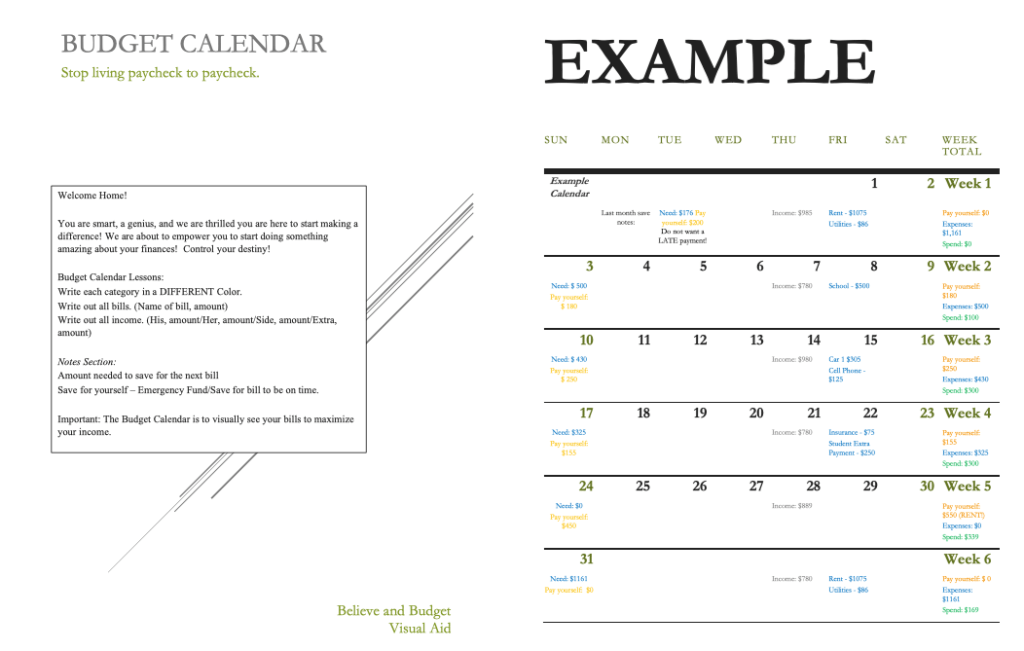

Start here with the free budget calendar.

1. Create a Plan

Just like weight loss, eating healthy, your job, school, and anything else in life.

You need a plan.

It was the “normal” to create this debt plan to go to school. It was for me, but once I figured out it should not be normal to be in student loan debt. I knew I needed out of it fast. Sit down and think about what you can do to get a little bit more ahead. Once you knock that first loan out, your plan will get done faster because you will be more motivated.

Similar to when you work out — it feels good — you are consistent with it until you stop. Similar to eating healthy — it makes you feel good. Think about those sweets you gave up and lost a pound how great you felt! This is how you will feel when you kill your debt.

Know how much debt you have — FIRST STEP!

Find a debt tracker you like and list all your debt.

I can relate to you that it can be scary and embarrassing, but I promise you — you are not the only one in debt. 80% of Americans are in debt — what does this mean 8 out of 10 people have debt! If you want to get out and you must create a plan.

Here is what my plan was…

“Get out of debt in 5 years.” — real life I got out of debt in 3 years!

Yes, my plan was that easy. I used a calendar for progress plus a debt tracker and listed all my student loans too.

We want to give you a free calendar for you to get started! We show you how to use it — it is simple, easy to use, and you can print it off or use it digitally. You can use it if you get paid weekly, biweekly, or monthly or even using just your savings while you find a job! It has been proven to work with all!

We hope you love it just as much as many others do!

2. Debt Snowball It or Avalanche it or Both?

1:1 Remote Budget Coaching

1:1 Budget Coaching Session – 45 minute budget sessions – Set up one budget – Follow up with one budget – Accountability to help you pay off your student loans

$159.00

Debt snowball – list all your debt smallest to largest. Do not care about the interest rates.

Avalanche – list all your debt from highest interest rate to lowest. Do not care about the amount.

Both – I listed my smallest amount with the 2 biggest interest rates then listed my biggest student loan debt with the highest student loan. Then went back to another small student loan to get me motivated again. Can there be a term for this too? Mountain/valley debt recovery?

Similar to the first workout — you are going to start on Monday and eat really good, but then what happens you might fall of the train…right? Well, if you are anything like me that usually is how it happens unless I am already in it for awhile and I am in my dedication mode!

If you hit the smallest debt first, you will be more motivated by the time you get to the largest debt you have.

Kill it!

Knock it out with me!

Hit a home run!

I actually did a little bit of debt snowball, and avalanche then switched it up because it motivated me to kill a big debt in the middle of my journey. As mentioned above…mountain/valley debt recovery helped me because just like when you are running. You start up a hill once you get to the top of the mountain you want to go down to a valley and get the momentum to make it back up another mountain. Yep me too! Our minds think a lot alike!

I killed a $1,800 debt first with a 6.8% interest rate.

Then killed a $2,000 debt with a 6.8% interest rate.

Then killed the big debt at $6,500 with a 6.8% interest rate. Yes, these were all the highest interest rates of mine, but it made sense to me.

Then went back down to a $1,000 debt with a 4.66% interest rate.

Do what is going to motivate you. After I demolished those small debts, the $6,500 one was one of my fastest to go.

So which are you going to do? Snowball? Avalanche? Both? You do you as long as it is to get out of debt!

Student loan debt is not good debt so don’t let anyone tell you that!

The Passionate Penny Pincher planner that helps me live a better life and organized life as a mom.

3. Live Below Your Means

I can tell you…you will be like everyone else if you do not live below your means. Personal loan, financing your furtniture in a house you cannot afford, car loan, another mortgage to do home projects, student loans, the list goes on… and on…

Personally, cars get me from here to there. Yes, I had a dream to get my dream car and you know what! I did, and I had the biggest buyers remorse after paying cash for it. I could not believe I bought a car with cash — that much out of my savings account that was for the car I was saving up for. But hey, that is off topic and that’s for another post.

Here is to say, I did not have a car payment. None! I lived with an old car I bought my senior year of college. I did not need a fancy new one. By the time I gave it to someone, it was 3 different colors. It had spots on it. I had a job for an entire year that I drove from store to store because I was working in the district and you know what… people saw my car. I would say to them often, “I am going to be paying cash for my next car.” “My car gets me to store to store. Why would I need a new one? Do you want to buy me one?” I remember telling my district manager this and he laughed at me, but then once I paid for my car with cash that was new…he bragged about me to everyone. He told people, “Yes, she bought that car with cash.”

How else did I live below my means?

Often I would say, “No I cannot go out this weekend.” My friends knew I was on a budget and most of the time they would work around me. We would go to someones house instead of go out without a cover and I could just drink water. We would go out for ladies night where there was not a cover. It is okay to say, “It is not in my budget.” Your friends will understand and if they do not… you do not want them to be your friend. Just to be brutally honest.

What else?

I buy a lot of things off of craigslist or facebook marketplace. I have moved to a lot of new places and sold my items I have bought to start fresh. I moved from Nebraska to North Caroline with nothing and then moved to North Caroline to Virginia. Yes, I bought all my furniture to furnish my apartment off of facebook marketplace and had a lot of people say to me, “Wow, your apartment looks great!”

There is more…yes!

I do not have the newest phone.

I do not have the newest clothes — I still have a pair of jeans I wear from high school!

I do not have cable and never did! I think that is pretty normal though now-a-days.

I do not have subscriptions – no to Fabfitfun! no to Stitch Fit! no to Fabletics! The only one I do have is Netflix for 12.99 a month and we are actually thinking about cancelling it because we have amazon prime that we pay for yearly to save on shipping, have 1 day shipping, so why not use their movies too!

Yes, you have to learn to live without a few things for a little bit, but then it becomes normal.

Right now with my family. We are learning how to budget with meal planning to save at the grocery store to only spend $400 a month for our family. When we were first married the first 6 months — we spent over $600 – $700 a month at the grocery store plus would go out to each spending $300+. We were spending over $1000 each month on food! YES, food! YES, crazy — even a pro budgeter makes some life mistakes, but we learn and I want to teach you off my lesson so you do not make the same mistakes I did!

You win with money faster than I did!

4. Live with Roommates

I lived with roommates for years!

I paid at the most $500 for rent. At one time I was paying only $300 per month. When we first moved into our RV we paid $360 for rent. Currently, we pay nothing for rent by work camping and traveling the country.

Why?

Because I lived that lifestyle of being “house broke” it is not fun. I spent almost $1,200 on my apartment with utilities. I loved the lifestyle being close to everything. I loved being able to have people come over and just walk places, but there is more than being house broke. I think God placed me in this situation for a year to be able to talk to others about that lifestyle of being house broke or apartment broke.

I do want to tell you something…even better!

I was not any happier living in the $1200 apartment than I am now living in my tiny home for rent free and volunteering our time. We fell into this opportunity and it has been a blessing.

Living with less is the best life.

“How to Get Through These Hard Times with the Unknown!”

We share secrets with you to win with your money plus how to have a successful day!!

5. Create Multiple Sources of Income

A lot of talk about creating multiple sources of income and how you can do it. I want to start with telling you it is just for a season to get you out of debt and start dominating your life.

Personally, I work 4 jobs – at the grocery store, baseball stadium as a cater, babysitting gigs, plus I also taught Jazzercise as early as 5:30 AM! I remember holidays such as 4th of July — I would start at the grocery store at 6 AM work there 6 AM – 2:30 PM and then go to the stadium and work 3:30 PM – 10 PM. It was okay for me because the stadium job was with my friends and it was working with being social. Plus I was able to network with a lot of people who would cater in the suites.

My multiple income now are my dividends that are consistently being reinvested into the market. Sometimes I look at my income and see $50 -$150 dividends coming to me. You might be thinking, wow that’s crazy and it is because I got serious in investing. I put a little away each paycheck and now I have my husband doing the same thing. He loves it — yes you take home less money, but in the long run it is amazing!

What kind of multiple sources of income can you create?

Remember you can do it and imagine the difference you can make in your family.

Do not have a job right now? Let me tell you another secret… you are not alone. If you go work somewhere to make a little bit of income for now, you are being strong, you have courage, and you are smart! It does not have to be your forever job. Let me say this again — it will not be your forever job! Maybe you will meet someone to take you further than you were. You will make a bigger step in life! Believe in it!

6. Call the Student Loan Company each month to place an extra payment on the principal.

Yes, call the company and ask for your student loan payment that is extra to be placed to your principal. Did you know if you do not call and ask this they will put it towards your both your interest and principal plus they will split it up between all your loans. Making it even harder to kill your student loans!

You must have a plan when you call.

I always called and said this, “Hi, I would like to make my additional payment towards my $X amount loan. Please place this payment to the principal only.”

How do I know this because I worked at a bank and saw people do it towards their mortgage. People could pay more for their mortgage too if they place their extra payment and it would go all towards the entire lump instead of just killing the principal. The principal is the main sources of the loan. Therefore say you take out $5,000 loan and it has an interest rate of 5%. You want it to just go to the $5,000 original amount you took out instead of a little bit to $5,000 and the interest that your 5% has accumulated.

7. Track Success Each Month

This is the wonderful part and should make you excited!

You are slashing your debt.

You are killing each loan!

You should want to keep track.

We did this every month and still do this to this day. We still track our success every month. I know what each account has in it since 2015. Yes, for over 5 years I have kept track each month my success because that way I know where my money is. What it is going to and where we are building our networth.

Remember that when you kill your debt. You now do not have a negative net worth, but a positive networth!

We have increased our networth by over 100K in 5 years!

You are making a difference in your family tree. You are accomplishing something many people do not because they think it is “normal” to have debt.

More Articles You Will Enjoy:

- Stay at Home Parent?

- 10 Things to do Differently with your money this year!

- 5 Financial Books that Will Change Your Life

8. Subsidized vs Unsubsidized Loans

Know the difference.

Subsidized accrue zero interest while in college. Saving you money!

If you can kill the subsidized loans while still in school or during the 6 month period after you graduate you will win! You will not have to pay interest. I made the mistake of keeping them to pay off last. I wish I would have had someone tell me to pay these off within the first 6 months, but I didn’t.

Unsubsidized accrue while you are in college. These are similar to any other loan you would take out. Make sure you are always paying your minimum payment and crush these after your first 6 months. Remember to pay off your subsidized loans first within the first 6 months to win!!

1:1 Remote Budget Coaching

1:1 Budget Coaching Session – 45 minute budget sessions – Set up one budget – Follow up with one budget – Accountability to help you pay off your student loans

$159.00

Like this post if you are going to get out if you want to change your money situation.

Learned something new? Pin the article to share with someone you know who could benefit from the read.

Share it and pin it to your Pinterest board.

Want to chat with us personally about your situation… email us!

You were looking for advice about how to pay off your loans fast was how you came across us and I am so thankful for you to read my article and support us! Continue to stay in touch with us!

You are amazing and we want to be able to help you.

I always have thought if I can help one more person get out of student loans like people helped me.

When I was starting to get out of debt — I bought items to help me make a foundation for myself. I still buy items I believe that will help me grow and build my net worth.

Whether you have not starting paying off your student loans or you have paid off a little bit of your student loans we have a debt tracker for you!

We want you to subscribe to our blog to stay tuned into the journey! I promise we don’t spam you.

Whether it is tiny living with a baby, budgeting to learn to save more/paying off debt, living your best life, and enjoying what God created us for! Life is just beginning!

Join us also on instagram at believe.and.budget!

Sharing is caring:

12 Comments on “How I paid off 32k of Student loan debt fast!”

We are the Maloneys!

We are here to help you live a better life by believing, budgeting, and growing your networth!

We paid off 112k worth of debt in 6.5 years, cash funded our $10k wedding, saved $10k for our baby, paid for 2 cars with cash, and grew our networth to six figures!

We travel the US in our RV and create handmade jewelry!

GET YOURS TODAY!

1:1 Grocery Budget Coaching

Set up a 1:1 grocery budget coaching session to get a personalized plan on how to save at the grocery store!

$159.00

Free 15 Day Money Inspiration Devotional

{kind=link}

{kind=link}

Pingback: 15 Future Friendly Good Money Habits to Teach Your Kids – Believe and Budget

Pingback: 5 Steps to Keep You Going In The Middle of A Mess – Believe and Budget

Pingback: How to Organize your Budget Emotionally – Believe and Budget

Pingback: Don’t let your student loans get you down! – Believe and Budget

Pingback: Refresh Yourself. Create New Years Resolution For 2021. – Believe and Budget

Pingback: How To Change your Language about Money! – Believe and Budget

Pingback: 4 Lessons My Wedding Ring Debt Taught Us – Build Your Marriage On a Good Foundation – Believe And Budget

Pingback: How to spend less on your groceries per week – Believe And Budget

Pingback: How To Change your Language about Money! – Believe And Budget

Pingback: 5 Things I Learned Living Tiny and Traveling the United States – Believe And Budget

Pingback: 10 Things To Do Differently With Your Money This Year! – Believe And Budget

Pingback: 10 Things To Do Differently With Your Money This Year! – Believe And Budget