Believe And Budget

Money Talk with The Maloneys

5 Ways to Save for an Emergency Fund

This post may contain affiliate links, and they are no cost to you!

People often ask me, “How do you save up for an emergency?” “How do you have extra money saved up?” It is hard to save up if you are not used to it, but you can CHANGE IT! I always tell people you have to be creative and now is the time to be creative. It takes 30 days to form a new habit, why not have it be one you can benefit from for the long run? I know you can do it! Hundreds of people just like you have turned their spendings into savings, which brings me to the first way to save up.

1. Turn Spending into Savings

During your monthly budget, you get to plan out where your money goes. Tell your money where it goes just like we tell our spouse what to do and where to go. Kidding! Well…kinda? Personally, I love this part of budgeting! It gives us the freedom to go shopping — like when Old Navy has their 50% off everything sale! But this article isn’t about shopping, it is about finding the money to turn it into savings.

Join us to learn more:

Here is what worked for us and many of my client and I am sure it will work for you too. I ask myself these questions…

- What do I value?

- I value the Lord and go to him for all my finances. In Proverbs 27:12 it states, “A sensible man watches for problems ahead and prepares to meet them. The simpleton never looks and suffers the consequences.”

- Savings for an emergency and not having to worry or take out?

- Personally, if I felt lazy after work I would choose take out, but I think not having to worry would be better. I hate when something comes up and I am not prepared for it financially, so definitely savings.

- Happiness for the long term or a short amount of time?

- Easy answer for me — happiness for the long term. I find happiness for the long term, because we are just passing through earth, but I do not want my family to have a burden when I leave the earth. I want to make sure I leave them financially set to pay for my expenses when I pass away. I have seen many times family’s suffer financially because of a loved ones death.

- The feeling of security or the feeling of greatness for the short term with shopping or buying something?

- I learned in college that humans need a feeling of safety always. It is number two in the Maslow hierarchy of needs. The first is ensuring we have basic needs (shelter, food, sleep, water) and then safety. It allows me to have control in my life and I am definitely a type A who needs control and order.

Download our free ebook:

“How to Get Through These Hard Times with the Unknown!”

2. Set Up an Automatic “Bill” to Yourself

This is pretty easy to do now with online banking. We use Capital One 360 because I can set up several funds to save for. Examples of bills I have done over the past decade. The first automatic “bill” to myself was the emergency bill like when my car used to break down, the unexpected came up, and even with the coronavirus and out of no where we do not know what is going on.

Also, we have pretended to have a car payment. I deep dived into this when I did not have a car payment anymore, and I set up an automatic “car payment” to myself in my auto savings fund. Currently, a small “house payment” for our house fund.

Ally.com has a system similar to Capital One 360 where they have “buckets” for several savings and its in 1 account.

2. Downsize and Sell

We recently did this — it has been awhile since we moved tiny and downsized our lives, but we find outselves alway downsizing! We made over $1,800 for downsizing our stuff when we first moved tiny. We sold our items on facebook marketplace.

Make sure you take a good photo of the items plus you will sell it if it’s marketed well. I always suggest to list it higher than you want to make off of it, so you leave negotiating room. I buy a lot of my items off of facebook marketplace and even found myself selling it for more than I bought it for! Yes, I made money off of items!

Even though we live tiny, we often find ourselves still downsizing and selling items. Last week, we sold Tom’s old chests for $20 to a college student traveling home and needed storage. It is a perfect time to do it. Someone else’s trash is another’s treasure!

Don’t forget to let us help you level up your finances in back to basics a money foundation course to move you up! No matter where you are in your finances. God can use us to help you!

Check out our money foundations course Back to Basic class!

Classes are open now!!

4. Unexpected Income

This happens to us somewhat often, to be honest, and I believe it is because we give monthly. God states in Luke 6:38 “Give, and it will be given to you…” I want to share some items we have been blessed with recently. Last year, we paid for the tuxes for the groomsman as a gift from us and we were blessed with finding a place to park our tiny home for a cheap amount (360 per month!) We also gave extra to our pastor for marrying us and we were blessed with an amazing amount of money for our wedding and we even got a free night stay at the beach on our honeymoon. These are just a few examples of how God has blessed with unexpected income with giving more.

The unexpected income can also be bonus’s, raises, tax return (even though you want this to be as close to zero as possible). We receive our bonus in March so this was a nice cushion for us, but I always ask God who I should bless and give 10% to 15% of it to someone else who needs it more than I do. For raises, I find this the easiest to add to your savings by 1 -2 % and not notice it by either adding a percent to your emergency fund or even your retirement account. This can be done in your direct deposit.

5. Side Hustle

How to make money other than your full time job. I did this a lot when I was trying to get myself out of debt right out of school. I made sacrifices. I worked a lot and missed out on family events, but my family knew I would work so we planned other days to get together. Personally, to beef up my emergency fund I worked at the local baseball stadium, the grocery store, babysat, and taught Jazzercise.

What about if you found a side hustle of watching children while the essential workers have to work crazy hours. Most daycare centers are only open 6 AM – 6 PM, and most essential workers have to work 24/7 including weekends. Another side hustle could be using your hobby’s as a talent and selling it. My husband sells his jewelry on Etsy — check it out! Another side hustle could be working at a retailer like Amazon or Kroger until your job comes back around. Side hustles are just for season of life to get a jump start on a goal like saving an emergency fund.

These 5 ways to save for an emergency fund are tried and true ways I saved up for an emergency fund. My husband even completed these 5 steps to save up his emergency fund before we got married! I encouraged him to use his creativity to sell his necklaces and he continues to sell them consistently even though we have our emergency fund 100%. As I said in the beginning, it becomes a habit and it makes you feel good about what you’ve accomplished that you just want to keep on doing what you are doing to save and make a difference in what you believe in.

Luke 14:28 For which of you, wanting to build a tower, doesn’t first sit down and calculate the cost to see if he has enough to complete it? A verse to remind us we should sit down and calculate how much you should save for your emergency.

Learned something? Pin it!

Liked the article? Pin it!

Motivated to save up for an emergency? Pin it!

Let us know at believeandbudget@gmail.com how you’ve saved up for an emergency yourself!

We want you to subscribe to our blog to stay tuned into the journey! I promise we don’t spam you.

Whether it is tiny living with a baby, budgeting to learn to save more/paying off debt, living your best life, and enjoying what God created us for! Life is just beginning!

Join us also on instagram at believe.and.budget!

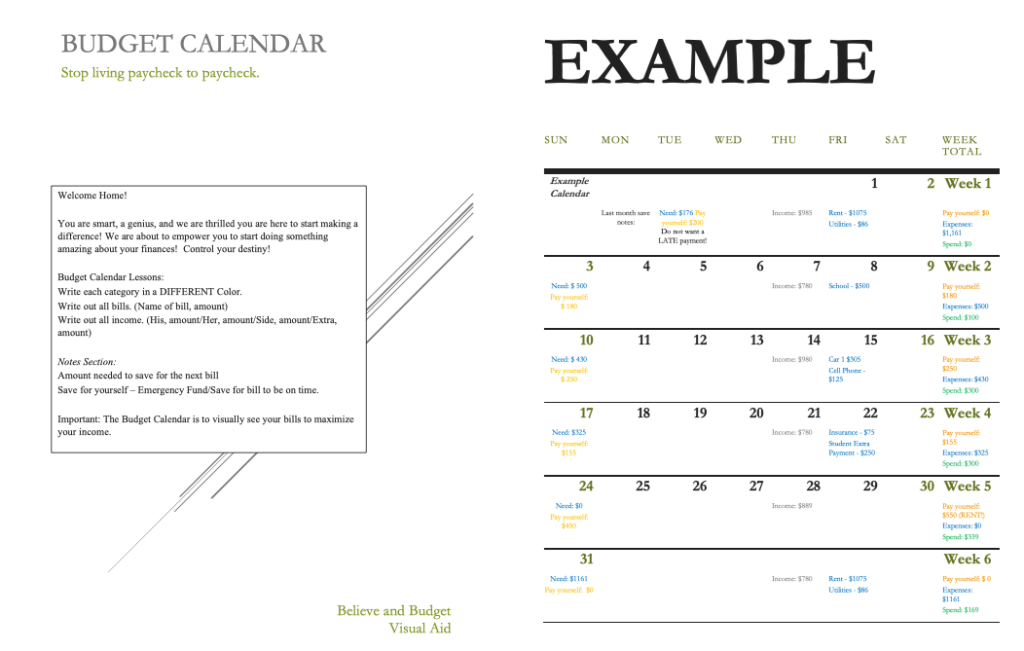

Make your budget easier by downloading the free budget calendar.

Sharing is caring:

Money Discussions before Engagement

Is it your dream to marry someone who is financially savvy?

Is it your dream to not get a divorce because of money problems?

Do you want to know what they want long term with their money?

These were often in my mind when I had a boyfriend. All my friends and family knew I wanted to marry someone who was financially savvy like me. I wanted someone who would work with me on saving up for our dreams. Make our dreams come true together. I wanted someone who would sit down and do the budget with me and make agreements on our financial world. Often financial matters are hush hush, but why? That is crazy to not know what they are doing financially before you say, “I do”.

“So I’m asking you, my friends, that you be joined together in perfect unity—with one heart, one passion, and united in one love. Walk together with one harmonious purpose and you will fill my heart with unbounded joy” Philippians 2:2

Have one intention with your future spouse be united in all this includes money as one. It is selfless.

Here are some tough conversations you should have with your boyfriend before you even think about engagement:

Start small conversations

Make sure you truly trust your partner.

If you care about your money and how you save and spend, I am sure it will be easier for you than you think. You will notice their purchasing habits when you are dating. I would not recommend talking about this as you could see it as a red flag if you do not agree with it. However, some boyfriends do it because that is how they are showing their love for you. They learned this from their parents most likely. If you do not have a love language of gifts, tell them! Maybe, your love language is acts of service this requires no money. Such as opening your car door, doing your dishes after cooking a homemade meal. You will think about how much money they spend on you when you go out on dates. This is also something you do not talk about, but you notice it.

You will probably know what kind of car they drive. This could start your small conversation.

For example, they drive a nice care…”Oh, I like your car. Did you pay for it? Did you get it as a gift? Did you finance it?” These are only examples for you to start the conversation. You can also tell them what you did money wise with your car. “Paid cash for it.” “My parents gifted me 1 car and I still have this car.” “I financed it, but paid it off fast to not have a car loan.” They may value their cars, and if they do this may not be the small conversation starter.

Find out what they want long term.

These are easy money conversations because it is talking about your dreams!

Do they want to live in a mansion, a tiny home, or a ranch style home? When do they want to retire? What do they see their retirement look like? These will all help you in the money conversation.

For me, I often told my boyfriends “I want to live tiny to be able to save up cash for a house.” “I want to live tiny to be able to live for experiences rather than stuff.” “I wanted to travel the world.” These are all ways I talked about money in the beginning.

Talk about Values in Life

Do they believe in being truthful? This is a big one because it is important to be truthful about the amount of debt one person has. I have heard stories where people lie about the amount of debt they have and then they come to buy a house together and cannot be approved for a loan. You want them to be trustworthy.

Do they believe in love? Love of what? Love of their family. Love of their money. Are they willing to share their money with you if they love it too much?

This will help you determine if their money goals are they same as yours. I often said, “I want to be a CEO of a company.” “I want to be a millionaire and I will do it with or without you.”

Health

Know each others health scenario.

This is an important topic to talk about too because if they do have a chronic illness or something they have to go to the doctors for consistently you will have to budget into your future.

You will need to think about good health insurance.

You will need to think about all of those expenses.

I have contacts that I have to get yearly prescriptions, and both my husband and I have fake teeth. We might have to get them redone in the future which we are saving for in our health savings account monthly.

Debts

It is important to be honest about what debts you have. Whether it is student loans, which 98% of people have. Car loans is another discussion to have. Personal loans. Do you have a credit cards with debt on it? These are all debts that are to be discussed to be open about money.

My husband knew I was debt free, and I wanted him to be debt free too. He had his personal loan for his car and student loans. He was actually upside down on his loan, but then one day his car broke down. That is when I decided to give him my car that was 100% paid off. He paid off his old personal loan for the car and sold his broken down car. He always tells me that is how he knew I was going to be his wife.

Be honest about your debts with your significant other!

Income

You will most likely talk about your income when you are close to getting engaged and have a life together. If you know you make more than your significant other, are they okay with this? It is normal for women to make more than men today. That is awesome, but would they be okay with this? These are conversations you need to have.

If you are going to start a family, talk about income this way as well. Would you want to stay home? Would you want your partner to stay home with the kids? Could you live off of one income or would you need two incomes and have the baby go to daycare? Day care is expense — $1,200 – $1,800 a month for a baby in the city!

Credit Scores

Your credit score is not a secret when you get married, so it should not be when you are about to be engaged! Why? What happens when you want to buy a house and your significant other has a bad credit score? You would not be approved for our mortgage. Remember you want to be able to use your credit score to get discounts on things like insurance, mortgages, etc.

Financial Goals – Big and Small

This is the fun topic to talk about with your significant other. Big huge financial goals what are they? A dream house, a boat, a dream car, etc. Being able to put your kids through private school or not.

Small financial goals could be saving up for Christmas, having an emergency fund, saving for a vacation instead of putting it on a credit card.

Joint vs Non-joint accounts

As the Bible says, you are united and this means sexually, but also includes your emotions (one will lift you up when the other is done and vice verse), food, shelter, possessions, and other stuff including your banking accounts are one.

Ephesians 5:31 “For this reason a man will leave his father and mother and be united to his wife, and the two will become one flesh.”

When you get married not only are you united under the same roof, but also with your finances which is why it is very smart to talk about having a joint account. We have been married for over a year and talk about it all the time, but still have not pulled the trigger to do it. We keep track of all our finances on mint.com.

Size of your Ring/Cost of it

This is super important when you are starting to get serious about getting engaged or you know it could happen with the person you are currently with. Why? Would you like them to take our a loan for a ring that is the amount of a car? Or would you rather receive a ring that the person can financially afford?

Do you want a huge ring but one that is in their budget? You should not have them pay more than 2 months of income. Therefore if you make $1,000 a month you should by a $2,000 ring. If you make $1,500, you can pay $3,000.

You want to be smart about it. I know people who have proposed with a .25 cent ring and they are still married and have been for a long time, but knew they did not want to go into debt for a ring. When they could afford more, the spouse bought a new ring for her that cost more.

I know people who only buy the silicon band which is a frugal. We looked at these since we were both in the retail working with customers, but ended up not getting them.

My husband paid less than the 2 month rule and I am okay with that plus he knows I did not want to be in debt because of my ring. We discussed what I liked and I showed him lots of photos. I told him I liked vintage and emerald cut. I love it, plus he got it with a deal where it was no interest for 12 months. He was able to pay it off before we got married. If he would have paid the minimum payment though he would have ended up paying interest, but he calculated it so he did not. (He is a smart man — why I married him!)

All of these topics are good to have with your partner before you think about getting engaged. You want to be open about a serious topic with each other.

Learned something from the article? Pin it!

Liked the article? Pin it!

Know someone who is about to get engaged or married? Pin it for them to see it!

Don’t forget to get your free money calendar to help you with finances together with your partner plus meal planning has been added this year from your feedback!

Join us also on instagram at believeandbudget!

Whether it is tiny living with a baby, budgeting to learn to save more/paying off debt, living your best life, and enjoying what God created us for! Life is just beginning!

We want you to subscribe to our blog to stay tuned into the journey! I promise we don’t spam you.

Sharing is caring:

5 Best Ways To Be Content – Because It Is Cheaper Than Not!

This post may contain affiliate links, and they are no cost to you!

Ever struggled with being content? The thought of being happy with the things that are right in front of you. For example, your current car, if you take care of what you have you will find joy and contentment in it again. Go and vacuum it. Go and wash it. Go and make it stand tall. If you have had the struggle of not being content, this post is just for you!

1. Stop looking back at things that are over and done with.

I know you may want to change what was in your past, but you cannot change what has already happened in your life. You cannot go back and cure the credit card debt. You cannot take back the car that you bought brand new and get full value for it. No one can change the past!

What you can do though that can change your future is stop adding debt to your life.

Stop trying to think about the what if I had this. Stop trying to buy your friends or your kids love. It doesn’t work. Trust me!

I had parents who were divorced. It didn’t work at all. I decided a long time ago money cannot add to your happiness.

Contentment comes from inside you. Right now.

Enjoying the moment you are in with what you have already. Not with what was your past or what is in your future. It is up to you right now.

Have you ever wished for something that you have right now or you are living in right now? I have! I dreamed of living tiny and we’ve lived that dream! We have to remind ourselves to be content with what we had and that we chose to live that lifestyle! It was good. It was adventurous, but it also came with trials too. I had to find contentment.

2. Give up that same bad attitude

Always go back to I cannot do anything right or I will be happy when.

Get yourself out of thinking like that. It does not help!

I know, I have been there. In the moment when I was suppose to be the happiest. The moment that I wanted so badly, but the thing is that I’ve learned and want to share with you. It’s alright to start over. To start fresh.

To remind yourself, you will have a bad day. Your kid will have a bad day. Your spouse will have a bad day.

But with the grace of God, he makes miracles called days.

So when it’s a new day, make it a new you! Make it a new attitude. If you fail at it for a moment try again, and say at least I’m not where I used to be. I’m on my way!

1 Peter 3:11 “Give up your evil ways and do right…”

3. Follow the path of Gods way

Printable Bullet Journal Budget Tracker

What you get? ✓ Printable Bullet Journal Budget Tracker ✓ Helps with contentment and findin your blessings each month ✓ Help you budget with the frame of giving, saving, and spending. ✓ Will be downloadable within 24 – 48 hours. ✓Nothing is shipped.

$2.99

Sometimes we get stuck trying to come up with plan A, plan B, and even plan C! When really these are none of the paths we should go. We try and try and try again ourself and get frustrated. We get mad and stressed. When we tried to leave where we were living, we tried every single state, called every state park, every job that opened. And every door closed! Every single door! I was so frustrated.

Until we sat down and prayed and God made it so easy for us to just stay where we were and be content.

- He opened doors for us to have free utilities.

- He opened doors for people to help us when we didn’t want the help.

- He filled our broken hearts with love and friends.

- He filled our prayers with hope.

- He filled us up full! So full we couldn’t imagine it.

- He made it possible for us to pay off our RV 100% on one income. From an over six figures to less than six figures income.

I’m telling you listen from my experience.

God wants the best for you. He will have people reach out to you when you need it most. He will have you read articles you need most and fill you up with hope!

The lessons learned… there are easier ways. Take little steps towards God. He has a great path. Open your ears to him. Look up to him. The Holy spirit is right there with you waiting for you. You will be free!

4. Unlock the happiness feelings with a key of happiness

Unhappiness is easy. It can continue to come back so easy to be negative and unhappy. There was a point where we needed to hang out with different friends because they were not what we desperately needing in our life. We needed something else. It was not magical but hurting our life.

The key of happiness takes practice. Keep practicing. Go to a place that is a happy place for you. Hang out with people who make you happy and not people who you complain to. You don’t want those people in your life, but people who bring sweetness to your life. How does this add value to your life and add contentment? It does because there is a deeper issue that is making you unhappy. A deeper issue that is making you not content. You must find it and it might take a long time, but keep trying. Find the right key and open the lock!

Other Articles you will enjoy:

- How to Avoid Temptation of Life When Managing Your Money

- How to Help You On Your Target Shopping Trips

- The BEST Ways to Navigate Through a Storm

5. Put your stuff first. Care for it. Give it value.

We want everything right now. We want it to make us happy, but the thing is it only makes us happy for 5 minutes maybe an hour. The worlds been busting us from the start. People go to work to figure out how to get us to buy more. How to get them richer and make us come back for more. Over and over again. I mean look at this thing that recently came out… Afterpay, sezzle, Klarna, quadpay. These apps are buy now. Pay later. Or buy now and pay less now. Pay in payments. This is adding to our none contentment. It’s teaching us poor money management.

I know I get it its convenience to pay 4 payments of $27 instead the full time at once, but think twice when you do it. It is making the rich richer and the poor poorer.

One thing I’ve learned personally, nothing satisfies us more than the things that we already have. Caring for the things around us with love. Fixing up what we have. Loving what we have before it is loss and too late.

I remember one time when I wanted this new car and I even bought it, but I was still in love with my old car. I took care of my old car with love, tender and care. The weird thing is my head turned down the new and the dream I had. I enjoyed being content with the old! Believe me you will be surprised for yourself!

I remember that I’m small and my story is just my story, but I know the big guy uses it to speak to others. I struggled with being content during our money journey, and if this article didn’t help you. It sure helped me when I needed it most! It reminded me I have everything I will ever need…God, God’s plan, and to trust God with it all! Those 5 things helped me remember this today and brought me back to my place of peace! So I thank you for reading, sharing because God can use my story you continue to help the hurting.

1 Peter 3:11 continued… “…as you find and follow the road that leads to peace.”

Did you know depression has increased over 50% in the pandemic?

Pin this post for a friend, because they secretly need it too.

Like this post, if this inspired you.

Like this post, if you struggle with having contentment.

Don’t forget to let us help you level up your finances in back to basics a money foundation course to move you up! No matter where you are in your finances. God can use us to help you!

Check out our money foundations course Back to Basic class!

Classes are open now!!

Sharing is caring:

4 STEP PROCESS TO CREATE A FINANCIALLY STABLE JOURNEY!

4 Step Process

Complete this 4 Step Process to Create a Financially Stable Journey.

If you have followed us for awhile you know that we stay on track with these 4 easy steps to build our net worth month after month.

Free budget calendar — Download it today! You will receive one for the new year soon!

1. Believe

You must believe that you are not the reason you have the income you have or you have gotten to where you are because of you. It is because God has a plan for you and He will make it possible for you.

We have not reached being debt free because of ourselves, but because God increased our income. He decreased our debt. He gave us opportunity and opportunity and more opportunity. He closed doors that were not suppose to be there. And opened other doors that where better.

When the times and season where rough. We prayed, prayed, and prayed, but not only that we thanked him for what he had done in our lives. Thank him for the little things that do not mean much to you, but to another person means everything! If you want to check out the blog post about starting out of day right read it!

- Have faith and know God’s way works

- Give from your heart

- Animal, Hospitals, Diseases, whatever you believe

- Believe in yourself you can do it day by day

2. Budget

If anyone has told you that budgeting does not work, please do not listen to them. They are probably broke!

Budgeting works. Why? How? Because you have a plan for your money. Because you have goals. Have you ever been at work and not had a plan to do for the day? I bet that day you did not accomplish much or you looked at the clock it was 5 o’clock and said, “Wow, I did not get what I wanted to get done today.” Why did that happen? Because you did not have a plan. A budget is just a plan for your money that is it, and it works.

Do you think Warren Buffet budgets? Hell yes! Did you know that he is one of the top millionaires that donates! Yep! He is! He budgeted to donate that much money too to things he believes in, which brings you back to believing our first step!

- Monthly – Create a plan

- Weekly – Follow up with your plan

- End of Month – Follow up with plan and see where improvements need to be made

3. Pay Debt

Debt it is rough. It causes people to lose sleep. It causes people to get divorces. It causes so many horrible things well besides your credit score. Oh, America!

I challenge you to talk to someone not from America and see what they think about America and how to “live” the American dream. It is all based on debt and credit scores. This should not be the case, but it is.

I challenge you to pay off all your debt student loans, consumer debt, credit cards, refinancing loans, car loans, boat loans, etc.

God made us to not be slaves to the debtor, which did you see that. He wants you to believe and he will bring your net worth higher! Are you trying to do it all yourself? Or you believe God got you! Do you have faith?

- Pay more than the minimum to increase your net worth

- Find ways to earn more money

- Discover a way out fast

4. Save Money

Matthew 25:14-30 – the parable of the three servants.

God wants us to save your money that he gives to you and invest it to double it. When you are faithful with his money and a small amount of it. He will give you more and more of it. He will give you more responsibilities.

- Start with $1000 in your Emergency fund

- Increase your Emergency fund little by little each month

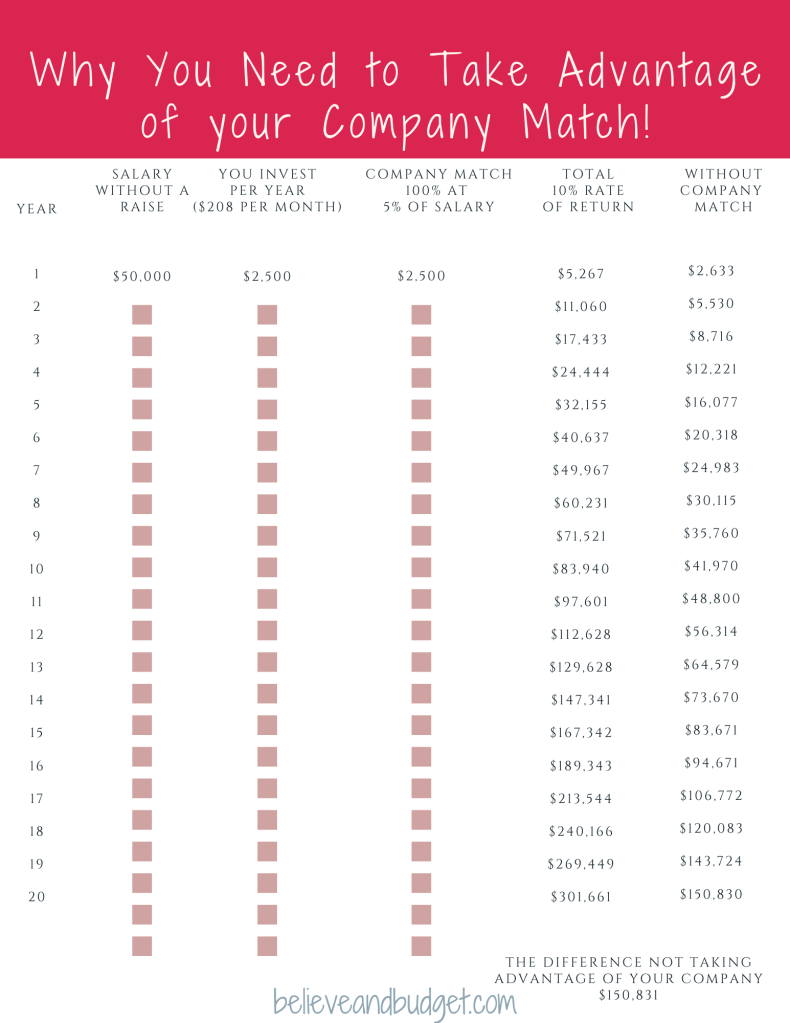

- Invest your employers match plus a little

Like the post, if you find one of these steps to help you in your financially stable journey!

Pin to help out another friend with this easy process.

Pin to remind yourself when you are having a silent season.

Make your budget easier by downloading the free budget calendar.

Sharing is caring:

Starting a family? — a Baby Fund — it is a must!

Thoughts of starting a family? Want to bring a child into the world?

Did you know hospital cost for a baby at the hospital is costly? Expenses start right in the beginning of it in the first few minutes of their life at the hospital. Epidurals alone are costly!

My husband and I agree’d we would set a goal and start putting away money for a baby fund.

Ways we were able to save up:

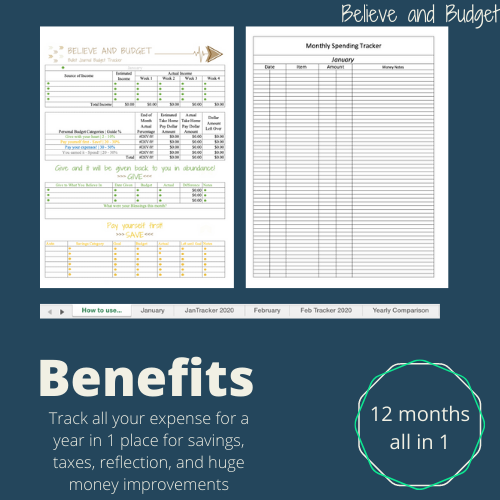

- Using the Yearly Excel Bullet Journal Budget Tracker

The yearly excel bullet journal budget tracker has 4 different areas of the bullet budget tracker. It has a section for giving, savings, expenses, and spending. The section to make our baby fund successful was the giving and savings. To get yours now and use it for your savings goal, click here.

Looking back on our giving and savings areas, when we gave to others in a way of finances our savings also grew the same or even doubled. It is like the Bible verse Matthew 25: 16 – 21. It talks about how God gave the servant 5 coins and it was doubled. God asked the servant what he did with them and he told him it was doubled. He told the servant he was a good and faithful servant and that he would put him in charge of much more, and to also go with him and share the happiness. Remember to flip it quickly — if God gives you something like a raise, a good bonus, something worth of value unexpectedly to give something quickly to share his blessings and your happiness.

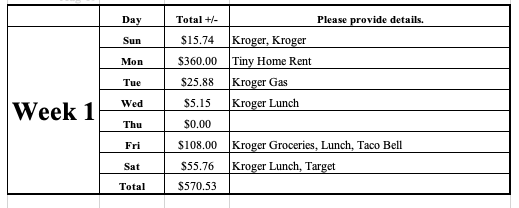

- Using the Daily Spending Tracker

The daily spending tracker allowed us to see where we were spending the most money each day. It is an easy way to see how many non-spending days you have and to see where you are spending the most money. Our daily spending tracker showed us we were spending money each day at Kroger since we both work there. It was crazy! $5 here and $10 there — it adds up!

This was a huge part of our success to tackle the area where we were spending the most to be able to save for the baby. Need to find out where you are spending the most money each week? The daily spending tracker is a helpful tool!

- Being the Bag Lunch Budgeter

Which brings us to the the bag lunch budgeter — this article gives details into ways to make bagged lunch cool. Personally, I had to convince my husband to get on the same page as me to bring lunches to work. I started to make him lunches and put little love notes in them as surprises. He loves it! I also showed him the savings we would have if he switched to bagged lunches. Win, win in my book and he was convinced! Once I was pregnant and not getting up early to pack him lunch — he packed his own lunch because he saw the savings that came with it. Successfully, we saved up $10,000 for our baby fund!

- Having a goal and date to save up by

We knew the baby was coming in January, so this was an easy check off for us. However, if you don’t know where to start. Think more about what you want the goal for is it for creating a car fund to pay for it with cash and never have a car payment again, is it for a family vacation for the summer, is it for a paid in cash Christmas, or is it for your future? When you know the goal it is a lot easier to come up with the date because as you read.. summer time – we want to take a vacation; Christmas, so this would be 100% by September to start the shopping; future, when do you want to retire?

- Setting milestones to celebrate

Make savings fun by creating a celebration whether it is a treat to not cook dinner for the evening, going out for happy hour, a spa day, treating yourself with chocolate, going for a coffee with a friend, or even just being thankful and celebrating with the good Lord!

Celebrate the hard work, the dedication, or the results you did amazing!!

Here was our WHY on saving up for a baby:

- A new reliable car

We did not want to keep the cobalt, a 2 door car, since it was not going to work for our family. We needed an SUV just in case Ember came in a middle of a snow storm. Last year, here in Virginia it was snowy and cold. We needed to know we could get out of our drive way since it is steep up incline. We wanted an all wheel drive for that reason. We knew we needed additional space for the car seat and not have to switch it from car to car. My husband has long legs!

- Family

We wanted to ensure we started out our small family without any stress. We needed to know that whatever came our way because “life happens” would be taken care of. It has also always been in my nature to save for events and if we were going to take this huge step I knew we needed a safety net.

- Doctor bills

We knew I was due in January, which meant TWO different years of deductibles for our health insurance. Our total max out of pocket is $5000 and thought we could max it out both years. Luckily, I had a smooth pregnancy and did not have any complications and it did not cost much in the first year, however the second year we have already met our deductible with Ember being born.

Added bonus we learned during the process:

- The savings

We saved 20% by paying our hospital bill before being discharged! It ended up being almost a $1000 in savings! Bonus in our book! Plus the fact we decided to have Ember without an epidural saved us a lot of money! An average epidural is over $2,000. We had a natural birth — not by planning it, but Ember came in 4 hours after my water broke and it went super fast! (It was not as bad as I thought it was going to be — and I dislike anything with pain, needles, doctors, etc) The IV was worst in my opinion.

I leaned on God a lot. Prayed. Listened to Klove radio to have her natural. My husband was a huge supporter as well. Breathing techniques — I learned the night before by @builttobirth You Tube video.

Overall, a baby fund is all about creating a routine of savings, setting a plan, and making it happen. You will be happy when you are able to enjoy the baby and not worry about the finances that come with them. You will be healthier because you are not stressing about finances. Be courageous and create a baby fund for your baby!

If you are not a subscriber to our blog, please join us in our journey! Tiny living with a baby, budgeting to learn to save more, live your best life, and enjoy what God created for us! Life is not over — it is just beginning!

Sharing is caring:

How to take advantage of your companies benefits for investing in your future

This post may contain affiliate links, and they are no cost to you!

Do you feel like starting to invest is hard? I can completely understand. I know many people right out of college feel the same way. You get your first job and have so much debt and you’re supposed to invest into your future, but you are just trying to understand the concept of investing and why now. Come with us to talk with you about how you can take advantage of your companies 401k and if you don’t have a 401k with your company you can open up a Roth IRA.

1. Company Match

The company you are working at right out of college will probably have a 401k whether you can invest in it right away it up to your company’s policy. Some do not allow you to invest right away.

Kroger did not allow me to invest until I was 21 and I started working there when I was 16.

Know what your company match is – it is FREE money!

It is very important to know what your company match is because you need to be taking advantage of it. Many people I have talked to do not do this because they “cannot afford it.”

Start small and grow it each time you have a raise or when you feel really good about your money situation you will be golden!

Where I used to work the match used to be if you contribute 5% and they would match 100% of the first 3% and 50% of the other 2%. Recently it changed and it is very rich match – Contribute 5% and they match 100% of the full 5%. This is 5% of the company adding to your salary in reality! Can you say… THANK YOU!

Whatever your companies match is please take advantage of it.

Don’t know what it is. Find out from your HR leader or your manager. I am sure they will know and help you out, which will bring me to the next point.

2. Ask your leader how to take full advantage of the benefits

One of my greatest mentors were my leaders in my career. They taught me all about the 401k benefit.

Do not be scaried to talk about it because it is your future you are investing in.

Let me tell you a secret.

You are not alone! A lot of people do not know about the benefits they are missing out on unless they ask.

Looking back at my experience in HR in the benefits world, so many people would ask and I was so excited and thrilled to help them out to help them grow their wealth.

When I changed roles and was a leader, I talked to even my department leaders about taken advantage of the benefits during our weekly close the loop calls because everyone needs to know and needs to be educated about the benefits.

3. Watch your money GROW!

How can my money grow? The magic of compound interest. Think of it as another place to get “free” money. Your money is working for you instead of you working hard for your money.

Let us show you the beginning of our start of investing.

From July 2015 – July 2016, I was busy paying off the last of my student loans to become debt free and did not contribute much to my company’s 401k. (If I could go back, I would have at least done a little bit like 3%).

In 2017, I started back up heavily, 6%, because I started reading books and articles about the magic of compound interest. I did an experiment with my own investment and want to share with you!

In 3 years, look at the growth. You can do the same!

My husbands’ looks a little bit different, but that is okay. That’s why it is personal finance. We all have our own journey. He started a little later, but has been investing in his future and paying off his student loans.

4. Talk to a Coworker!

My hubby is a great example of this…

When we first met he was not investing into the 401(k), I get you – you are thinking and you married this man? YES – he challenges me in other areas where I am not strong.

Anyways… I talked about it a little bit to him but knew I could not push it onto this decision. His coworker and my hubby then started talking about it one day at work, and they both started investing into their 401(k) together!

Now, my husband is investing more into his 401(k) and ROTH than I am and it is because a friend talked to him about it.

Do not be scared to talk to someone about investing in their future. They may need you to give them a little boost.

5. Invest into your HSA

Another good piece of investment with your company is the Health Savings Account (HSA). This is where you can place money into a fund where it is tax free now and you can use for medical expenses in the future.

To open an HSA, you have to be enrolled in a high deductible health plan.

My old company would allow you to keep $1,000 in the regular savings fund and then you can invest the rest! You know what I did, I invest the rest because why would I risk letting my money sit there doing nothing?

I had an executive who was my boss tell me the greatest advice and I want to share it with you all.

He told me, do not spend the money you place into your HSA. You may think you “need it now”, but wait until you are older. You will need more medicine, you will need more doctor visits, and you can even use it to pay for your Medicare and Medicaid!

To this day, I have listened to him and invest it for my future.

We did not even dip into it when we had our baby. We saved up a baby fund with $10,000 to fund our baby expenses.

Articles you will also enjoy:

- 4 STEP PROCESS TO CREATE A FINANCIALLY STABLE JOURNEY

- 3 TOP WORLD PANDEMIC BUDGET CHANGES YOU NEED TO MAKE TO BE SUCCESSFUL

- 10 THINGS WE TOOK OFF OUR GROCERY LIST TO SAVE THOUSANDS

6. Open a Roth IRA or an IRA

Your employer does not offer you a company match or a 401k option until after a year or even three years. Do not let them stop you from investing into your future.

Open an account with a broker. We use Betterment. I have used TD Ameritrade and Robinhood too. If you want an easy investment account, Betterment is for you.

You will want these accounts anyways when you work for a company and need to roll over your investments if you leave that company anyways. That way you do not forget where all your money is when it comes to retirement.

Leave a company. Take your money with you and roll it over to your outside investment account. Personally, I have done this with the companies I have left.

Listen here, if you think you do not have money now. You do not want to be in the same position when you are 80 or 90 years old and cannot physically work.

Start small. All eyes on you right now. Just kidding, but seriously.

Let it all out, scream, shout, and open it up.

Post it once you do and let me know, tag me in it! I will be your cheerleader!

I will dance and sing and have some drinks with you to celebrate! Even ask my sister, we partied hard for her 21st birthday. I also say I will be like my mom and party with my kids when they turn 21 and do a power hour! Why? Because life is FUN! Investing can be FUN too! Think of all the FUN you will have when you can have in your future!

Want to make life last forever? Start investing in your life!

If you learned something, like it.

If you want to let someone else learn, pin it.

Know someone who is young who would benefit from this, pin it.

Want to be happy in your future, like it.

Photo credit:

Sharing is caring:

Don’t let your student loans get you down!

This post may contain affiliate links.

Do you wonder how people get out of student loan debt and become debt free? This post will show 8 simple steps you can follow to get out of student loan debt and not get you down. Take the overwhelming number and crush it!

How I paid off my loans 3 years ahead of my goal!

My personal story:

I started paying off my student loans while I was still in school because I took a financial class called Financial Peace University through my sorority. The class was only offered to the greek students for free at our university!

Paid the unsubsidized loans off while I was in school because they accrue interest right away. The subsidized loans do not accrue interest while in school, added bonus, I waited to pay those off. I had a total of $32,000!

How did I do it?

I made living sacrifices.

At the time, it did not really feel like sacrifices since I never lived by myself. I would consistently live with others to reduce my housing cost. I lived with my sister for free, lived with my friend for $300 (I had the entire basement to myself and the garage) , and lived with a random person for around $350 in the middle of Raleigh, NC. As I was living a low cost, I was able to clear my debt fast.

It also helped knowing the difference between these two words: subsidized versus unsubsidized. Which I mentioned already above.

1. Check out this website and know how much you have while in school

This website, studentaid.ed.gov should tell you how much money you have taken out from the government. Many companies are compiled under here and it will help you understand the number for your debt free journey. You need to know by heart how much debt you have. It will help you conquer it!

Studentaid.ed.gov

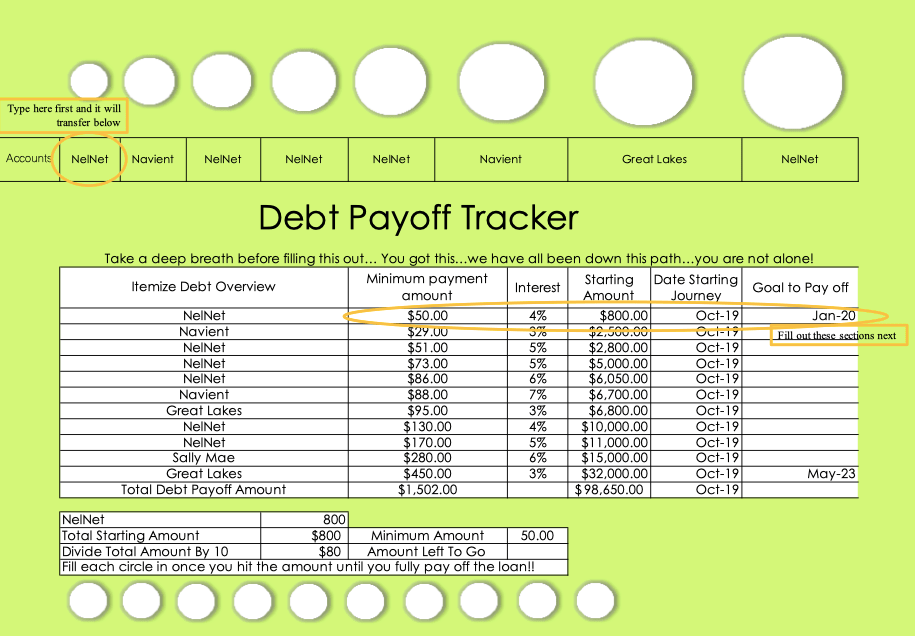

2. List the loans out the order you want to pay them

Most people recommend smallest to largest. It give you the momentum to crush your loans. As long as you have a plan to pay them off each month you are golden!

We did a bunch of different ways. I crushed the smallest, but then when I had tax returns or other surprising lump sum cash. I would crush a loan with a high interest rate.

3. Pay the minimum payment by auto payment online

Automate the process. It is the easiest way to crush your goal. You want to only pay the minimum payment automatically online though and we will tell you a little secret. The government doesn’t care if you pay more and they do not want you really too because they are making money off of you!

4. Do not pay extra payments online!

They also do not tell you…if you pay more through auto payment online that they equally distribute the payment to all your loans! Which makes it longer for you to pay off!

5. Call the loan company each month

Yes, I said it. Call the loan company each month to add your $400 extra payment. I tell you this because that way you can specifically tell them what “token” you want to pay off. Otherwise, it will take you longer to pay off your loans. We want you to pay them off fast! Fast is the key!

6. Pay extra to the principal

Be specific when you call the lender and tell them, “I would like to place $400 on the principal of token Nelnet it has an interest rate of 3.5% and it currently at $5,603.”

7. Feel good slicing each loan

You are in a journey. Remember to feel good that you are slicing each loan. We love that student loans are little pieces because it is just getting you ready to knock out your next loan you have to become totally debt free.

Other articles you will enjoy:

- How I paid off $32k of student loans fast!

- How I lived without an income for 3 months.

- Bagged lunch budgeter – Turning a habit to paying off debt faster.

8. Celebrate!

When you make a goal to clear out one loan. You need to celebrate! Celebrate that milestone it will make you feel good. It will show you who you are and what you are able to conquer! You are a BEAST! Congratulations!

And those are some amazing tips to get you out of student loan debt fast! They are simple and to the point. Think about that sacrifice are you going to make to delete your student loans fast?

Like the post, if you are in this process to dominate your student loans!

Did you know 8 out of 10 people that you know have student loan debt?

Like this if this post helped you.

Pin to help out a friend or two who has student loan debt.

Pin so you can refer back to when you need a reminder of how to pay off your student loans.

Make your budget easier by downloading the free budget calendar.

Sharing is caring:

5 Ways to Build Your Credit Score

This post may contain affiliate links, and they are no cost to you!

Do you want to learn how to increase and build your credit score, but don’t know exactly where to start? I have some realistic and practical ways for you to do it. I am living proof you can raise your credit score. I have done it. I have helped people do it and I want to show you through stories to help you know you can build your credit too for your next big purchase whether it is a home or a second home.

1. Call your Credit Card Company to Increase the Limit

This seriously works and it is easy to do. Call your credit card company and simply ask for them to increase your credit limit.

Script: “Hi, I am a credit card holder of XXX company and I would like to increase my limit.”

Once you get the increase limit do not use it. It will maximize your power to increase your credit score. The key thing is to not max it out – if you do there is no point in doing this easy step. You will have now less debt to your credit limit.

I will show you.

Say your credit card limit is $15,000, and you have spent $10,000 on your credit card. You call and ask for them to increase it, and they increase it to $25,000. Wow, look at that you are using less of your credit and it is better on your credit score!

The credit score thinks it is excellent to have a total available credit of $50,000+, so keep asking for an increase in credit and do not use it.

You can continue to pay it off and make progress increasing your score.

2. Pay off your Credit Card in Full Every Month

This may seem like a simple task, but I am here to tell you. People think it is the “norm” to not pay off credit cards each month. People think it is the “norm” to use only credit cards.

I want to tell you a secret — credit card companies do not want you to know.

It is not the norm to not pay off your credit card.

It is normal to pay off your credit card in full every single month!

So, if you have a balance on your credit card. You can and should pay it off! You can do it!

3. Leave your Credit Card Open

Once you pay off a credit card, do not close it. Leave that credit card open and put it in a drawer. Use it now and then, but not all the time. You will be successful building your credit.

It is a silly thing, but it really does matter how many accounts you have open and how long they are open for your credit score.

My longest account open is 11 years and it is considered good, but excellent is over 25 years! So most of us have some years to go! I would have had to open my credit card at 5 years old to have “an excellent” in this area.

If you’ve paid off your credit card, great! I am so proud of you – leave it open!

4. Use your Credit Card for One Category of Your Budget Only

This is key to a successful credit card usage if you are learning how to use a credit card properly.

I first got my credit card in college, and my father told me to only use it for gas. I was only going from school to work to home, and wasn’t going anywhere else really. I would fill up twice a month, so it would have maybe $80 on it every month. This built in a great habit to use my credit card, and then pay it off every month.

As I got more comfortable using my credit card and knowing I would pay it off. I changed the purpose for my credit card, and it became my big purchase credit card. I only used it for big purchases that were planned in my budget at the beginning of the month.

I would buy flights with my credit card that would cost around $350, but I had already had the money accounted for and planned for this big purchase. Paying it off in full each month. Plus I only traveled two or three times a year at this point.

Using your credit card for only one category in your budget works, and it has worked for me and many other clients I have worked with, which brings me to the next point.

I never used it for emergencies! This will only cause huge problems and cause you not to pay it off in full at the end of the month!

5. Get a Budget Coach

Hire yourself a budget coach. These are great investment!

I am thankful for my budget coach who helped me when I first started my journey. I mean no one teaches you all you need to know about budgeting.

- How to be successful in a budget.

- How to follow up on a budget and make adjustments.

- How to plan for big purchases.

- How to feel good about your money.

- How to increase your credit score.

- How to reduce your spending in an area and hold you accountable.

- How to make a good relationship with money instead of saying it will always be this way.

I will be the first one to tell you from experience. Hiring a budget coach is the best thing that ever happened to me, my husband, my family, and many other clients and their families who have worked with me as their budget coach.

I have helped clients increase their credit score by working with them in both my 1:1 Budget Coaching Session and my Back to Basic Course.

Here is a REAL testimonial for you:

Other Articles You Will Love:

- How to Spend Less Per Week on Groceries

- How to Change Your Language About Money

- I am Budget Ready, but I am Still Failing

Hope you have learned a little more about how to increase your credit score with practical ways. These have helped me and many other people, so cheers to learning and improving your life! You are on your way to improve your financial story!

Check out our Back to Basic class!

If you are a subscriber, we have an early bird special coming soon! It will fill up fast, be sure you get in now!

Like if you want to improve your credit score.

Like if you have a credit card.

Share if you know someone who could use this.

Sharing is caring:

10 Road Tripping Hacks to Save Money!

Summer traveling is right around the corner. I get it you want to travel even when the economy is not ideal and the inflation is high. How do we do it? Let’s learn how we save money traveling and how you can do it too!

Save Money the Old Fashion Way

Traveling is fun, but it can also be expensive when you just lost a job or when you are living on a tight budget. It also can be doable! You just have to use a few of our tips and tricks to do it! I am a queen of road tripping and saving money so let me tell you our ways!

Travel in your state

Living in new places makes this easier for us, but you can do it to.

Look up some parks close by or even better have a beach, mountain, river, lake or other outdoor activity. Travel to these places first.

We love to go to new trails. We use the app AllTrails to find new parks to go on hikes with the baby and the dogs.

Hey, my sister lives in the middle of nowhere. I am for real – a small town of 800 people! (My husband graduated with a class of 800!) They went to a new lake with 3 kids and it was FREE! The kids loved the day! The only thing that cost them was the gas to get there and packed some lunches!

Pack and buy food before you go

This was hard for my husband to adjust to and so when we first were married I became very lenient on this one too! We would stop everywhere to eat! It would end up costing us a lot more than I thought because we had a big budget for food! The freedom of being debt free right? Spending your money on whatever you wanted because you were debt free. Yes, this happened to me!

Now, since I am a stay at home mom and living off of one income we closed in the budget back to how I used to be before getting married. We pack food before we go.

The last trip we went up to see our parents. I went to Lidl and spent $15 for the food for there and back! Yes, I bought 5 powerades, ham, cheese, bread, chocolate trail mix, chips, and popcorn. I made 10 sandwiches for my husband and I. Yes, 10! I ate 2 and my husband ate 8. If I did not make that many, we would be stopping for a Taco Bell Break. Then of course we have our water bottles that we drink and can fill up too.

Fill up at a half a tank if it is cheaper where you are at

This is easy if you are planning your trip out. We know when we travel north from Virigina to fill up before we leave home. We fill up right before we leave the Virginia border and then again before we get up to Pennsylvania because man Pennsylvania has expensive gas and New York is even worse!

You can use apps like GasBuddy to track the gas prices before you leave and see where the smartest places will be to get gas.

Do not buy fast food or gas station items

This is a big one and goes a long with the pack and buy food before you go, but sometimes you are craving something you did not pack before you left. Repeat this over and over again. Do not buy fast food or gas station items! This is a huge money pit!

If you are going to go to a fast food place, you could only buy off the dollar menu but who wants that? Do not give yourself the temptation.

Visit free places

Search google for free places around where you live. We have traveled to many places close to us. We have the beach 2 hours to our east and mountains 2 hours to the west. We are pretty lucky on this and that’s why we live where we live. However, if you live someone like where I used to live, Nebraska, aka “middle of nowhere” You can still find places to go! Travel to a small town that you’ve never been to and visit their park. Drive around their town and look at the old houses. You can even walk around their town to get some fresh air. It is unique but that’s what we do in the city is walk around neighborhoods to check out the area.

Find unique places that are free to go to!

Enjoy the land

If you have been following us on Instagram, you know during quarantine we got out of our little tiny house every day and found a new trail to walk to enjoy the land. I do not like being inside for the entire day even before quarantine. Check out Quarantine with a baby in our Tiny Home. It allowed us to learn more about the land and the battlefields close by our house. I bet you have history around your house that you can adventure out to or even better you have unique rivers, forests, cornfields, etc.

If I were back at my moms’ house, I remember riding my bike every day in our neighborhood! We lived on gravel roads – I hated when the road grader would come through! Y’all probably don’t even know what I am talking about, but that’s okay.

If anyone does…please message me on Instagram and tell me or even e-mail me!

Camp or glamp

We glamp now. Well because we live tiny! I was just writing on Ember’s first year calendar “Embers first camping trip” and dad told me, “You camp every day.” Haha!

For real though, we used to go out on backpacking trips and camp in a tent. It was free! We would just bring our food, tent, sleeping bag, etc and go camping and it was so fun! You can do this too!

If you camp in a campsite most likely it will cost something, but not as much as a hotel. Even if you live in New York City, you can find camping if you get out of the city a little bit!

Other posts you will enjoy:

- Family is important – Flying doesn’t have to be expensive!

- Traveling Tips while Paying Debt!

- 5 Morning Routines for Success!!

Plan before you go to save

There is never a trip that I have not planned for before I have left. Whether it is food, gas, where I am sleeping, or who I am seeing. We always plan at least most of the trip and then leave a few days unplanned for relaxing or if we want to stay somewhere longer.

Planning before you go does save you money, so do it!

Yearly Bullet Journal Budget Tracker

On sale for ONLY $19.99 with this post no coupon necessary! Purchase today before it goes back up to the original price $24.99! The tracker will help you get a head start on your yearly budgeting. Planning for Christmas, start today with this budget tracker! Planning for a fall vacation? We know you planners will love this budget tracker! You will be able to change your life with it! All formulas are already included! You will feel financially free. You will feel a sense of worth! You will find it is easier to budget with this yearly template all put together for you!

$19.99

Pack all essentials before leaving

What essentials am I talking about? I am talking about toiletries — pack these do not stop to buy anything if you forget it. Do not stop and buy clothes if you forgot something it will just cost you extra money you did not budget for. Which brings me to another topic, do not just go to another city to go to a shopping mall. Unless you do not have the store at the shopping mall, but most of the time you will just get into trouble shopping because you will say to yourself, “I am on vacation!” “I am getting this and that, and oh yes, this too!”

Do not forget anything by making a list a few days before you leave

This helped us this last trip to make a list before our trip. As I have mentioned before, we live tiny so usually we just pull in our slides and away we go. This time my husband and I wrote down a list of everything we needed so we did not forget anything! Well, we did forget the masks because that is a new thing for us right now while I am writing this.

Things to write down: what you want to clean before you leave, food to grab out of the fridge, chargers, beauty items that you used the day of, kids stuff, dogs stuff, etc.

Write it down!

I hope you enjoyed the traveling hacks and learned a thing or two to do when you travel on your next vacation. There are always new places to see and do close to you and I hope you realize that! If you use these 10 hacks, I am sure you will be traveling more and more and spending a little less when you travel.

If you love traveling, like the post.

If you find that you will be doing more road trips this summer, pin this to your pinterest.

If you found a good hack, pin it to your pinterest to share it with a friend.

Thank you for being apart of our money family.

We love that you support us and if you have not subscribed to our blog yet. Please do! We do not spam you! You receive one e-mail each month that include freebies and goodies!

We could not do this without the guidance of the good Lord. We thank him as well.

Happy Money Hacking!

Sharing is caring:

How to shop your cupboard to reduce your grocery bill!

This post may contain affiliate links, and they are no cost to you!

Have a huge pantry full of food? A full freezer full of food? Stuff behind other stuff that you don’t know what to do with? I bet you have enough stuff in your cupboard to make dinners! Remember some of these steps might not all apply to you and that is okay! We all do things differently and that is okay! It is out here for you to learn our process of grocery shopping to help you in your journey to cut your costs on your grocery bill. My mom even proved to me that she could do it – she has minimal food in her home! I know you can do it too with these steps!

1. Step into your pantry or open your cupboard

Come on over to your pantry or your cupboard and physically look into what you have. This is your good luck charm. If you try to do it while you are at the store, it will not work. Trust me! You must take 5 minutes and physically do this.

We use everything from our pantry, cupboard, freezer, and fridge each week most of the time. You can do this too!

Sometimes we even make a meal off of just our condiments like our BBQ sauce or Salsa. BBQ chicken sliders and Crockpot Shredded Chicken Tacos!

2. Look to see what you have

Let your mind go. It does not matter what you have. It does not matter how messy it is. It does not matter how unorganized. You just need to dig through it maybe. Clean it later.

This is allowing you to brain dump recipes that are easy to make for you. Your money is going to thank you! Your money is going to appreciate these steps you are doing! You might not what you find! Maybe, some peaches from two years ago. Maybe some pasta? Blueberry jam that is still unopen. We have figured out dinner recipes from these odd ingredients. Keep reading to find out what we did!

3. Write down all you have

Digging deeper and physically write down all you have. It can be on a scrap piece of paper or we created a beautiful ebook for you – Meal Planning Ebook.

You do not need to take a bunch of time doing this. If you have a lot in your pantry, start small by focusing on the things you know you can use right away. This is the better idea instead of making yourself overwhelmed. Take a deep breathe allow this to be such a budget saver instead of a budget buster.

4. Google or Pinterest recipes you can cook with that ingredient

Remember that blueberry jam I had? I want to show you that we made it possible to use it up to free up space. This is really how we learned how to do this money saving hack because we live tiny and do not have very much space. Where are we taking you? To discover the best money saving grocery tip to help you too!

Do you have peaches from 2 years ago? How about a peach chicken salad? Or pork and peach tacos, ginger peach chicken? Peaches and pork chops? There are endless dinner ideas. Plus you can use them even for breakfast with oatmeal or jazz up some plain yogurt. You have nothing but millions of options!

Last one I am going to do for you and then I want you to do the same brain storming. Noodles. Odd noodles? Ideas are spaghetti, stuffed tacos, goulash, turkey and spinach stuffed shells, tomato and garlic butter pasta, or even one pot cheesy cheese pasta!

Be sure to look at all the ingredients so you know that you only have to buy a couple of items. If you have to buy a bunch of new items to make the dinner, can you substitute or just skip it and go to the next option. If you want to make this dinner in the future, save it to your pins and start looking for the ingredients when you find them in your budget or on sale.

5. Write down the dinners you are going to do

Now, here’s where it gets good! Give yourself everything you have ever wanted! A dang good savings on your budget! Write down the dinners you are going to make for the week!

Planning on eating at home 5 times this week perfect! Write 5 dinners down.

6. Put on the grocery list what items you need for that recipe

Once you’ve got your list of the items you have, the dinners you want to make off the items you have, now is the time to write down the other ingredients you need for the recipes. I am so proud of you so far! You are going to see such good things happen in your grocery shopping.

Key trick: Only choose recipes that need 2 -4 items to purchase

When you choose recipes. You want to choose real recipes that will help you not destroy your budget. Do not take away from your savings. You can remember that you can do this. I know this is a lot of information all at once, but take it step by step!

Recipes that you only have to buy 2 to 4 items.

Blueberry chicken recipe –

Need: Chicken

Substituted: Raspberry vinegar for balsamic vinegar, Dijon mustard for regular mustard

Had on hand already: S&P, butter, blueberry jam, basil

Guess what it turned out so good! It did not become a regular meal for us, but it did use up an ingredient out of our home.

Key trick: zero waste + Using what you have

We love not throwing away any food, and this definitely helps us do this by shopping out of our pantry. It comes even easier in our tiny fridge. It usually looks like this when we go shopping (left)

After our shopping trip and spending less than $100 a week. It looks like this (right). Yes — please do not judge me we like to drink beer — we call it good beer Fridays!

7. Distract yourself and stick to your list for the meals you are preparing

It is going to be the best thing for you, and you don’t even know it.

I understand and know how hard it is to stick to a list because in all seriousness my husband always tells me before I go to the store…”STICK TO THE LIST!” even I can confess that this is a hard step!

These 7 steps I know will help you shop your cupboard to bring your grocery bill under $100! We live tiny and still are able to do this with purchasing meat every single week! Most people think meal prepping and storing a bunch of food is the only way to do this, but I promise you it is not! We start over almost every week! You can do it too!

Like this post if you shop your cupboards to save money.

Like this post if it inspired you.

Pin this post to help someone else save money on their grocery bill.

For reading this post, we want to give you a deal for your purchase of our bullet budget journal to change your budget and give you an abundant life!

Classes are open now!!

Sharing is caring:

We are the Maloneys!

We are here to help you live a better life by believing, budgeting, and growing your networth!

We paid off 112k worth of debt in 6.5 years, cash funded our $10k wedding, saved $10k for our baby, paid for 2 cars with cash, and grew our networth to six figures!

We travel the US in our RV and create handmade jewelry!

GET YOURS TODAY!

1:1 Grocery Budget Coaching

Set up a 1:1 grocery budget coaching session to get a personalized plan on how to save at the grocery store!

$159.00

Free 15 Day Money Inspiration Devotional

{kind=link}

{kind=link}